Use a commercial mortgage calculator to estimate payments, balloon risk, and deal fit before you talk to a lender.

A commercial mortgage calculator matters the moment you stop asking, “Could I buy that property?” and start asking, “What would this loan cost me each month, and would this deal still make sense for my family?”

That’s a significant hurdle for a lot of buyers. You see a small mixed-use building, a storefront, a four-unit property, or an office condo. The listing price is one thing. The financing structure is another thing entirely. Commercial loans often have shorter terms, different amortization, and sometimes a large balance due later. A quick rate quote alone won’t tell you enough.

Used the right way, a commercial mortgage calculator gives you a fast first-pass answer. It helps you estimate payments, compare loan scenarios, and spot problems before you waste time on a deal that only looks good on paper.

This article may contain affiliate links, which means we may earn a commission at no extra cost to you if you choose a recommended tool or service. We only recommend tools we believe may help.

This content is for general educational purposes only. It isn’t lending, legal, tax, or investment advice. Always verify loan terms, underwriting requirements, and property-specific assumptions with a lender, broker, CPA, or attorney.

Quick answer: A commercial mortgage calculator estimates loan payments, interest cost, amortization, and often balloon payments based on inputs like loan amount, rate, amortization period, and term. It can help you compare affordability and financing structure. It cannot tell you your final approval terms, exact fees, reserve requirements, or whether a lender will approve the property and borrower.

Introduction and Quick Answers

A lot of commercial deals start the same way. You drive past a property with a for-sale sign, pull up the listing later that night, and wonder whether the payment would be manageable or whether the deal would strain everything else in your life.

That’s why a commercial mortgage calculator is useful so early in the process. It turns a vague idea into a rough financing picture. You can test whether a higher rate breaks the deal, whether more cash down lowers the payment enough to matter, and whether the loan structure creates a balloon you’ll need to handle later.

Quick answer box

-

What it does

A commercial loan calculator estimates principal and interest payments, and many tools also model interest-only, balloon payments, and amortization schedules based on loan amount, rate, amortization, and term, as shown by MortgageCalculator.org’s commercial calculator at https://www.mortgagecalculator.org/calcs/commercial.php. -

What costs it can estimate

A stronger commercial mortgage payment calculator can estimate monthly debt service, total interest, and sometimes a future balloon balance. More advanced models also help you evaluate DSCR, LTV, and debt yield, as described by Adventures in CRE at https://www.adventuresincre.com/commercial-mortgage-loan-analysis-model/. -

What it can’t tell you

It won’t tell you your exact lender fee stack, required reserves, final APR, legal costs, or property-specific underwriting decision. -

Who should use one

It’s a smart first step for small business owners, first-time commercial buyers, multifamily buyers, and investors comparing loan structures before calling a lender.

What Is a Commercial Mortgage Calculator

A commercial mortgage calculator is a financing tool built for business and investment property loans rather than standard home loans.

That distinction matters. Commercial mortgages often don’t behave like residential mortgages. You may have a shorter loan term than the amortization period, which can leave a remaining balance due at maturity. A better commercial property mortgage calculator accounts for that structure instead of pretending every loan fully pays off in one straight line.

What it typically asks for

Most calculators use a version of these inputs:

- Loan amount

- Interest rate

- Amortization period

- Loan term

- Payment type, such as principal and interest or interest-only

Why it helps

The value isn’t just the math. The value is speed.

You can compare financing scenarios without waiting for a full quote. Raise the rate. Change the amortization. Increase the down payment. See how each move changes the monthly payment and how much risk you’re taking on later.

A commercial real estate loan calculator is best used as a decision filter. It helps you decide whether a deal deserves deeper analysis or whether it should go in the “not now” pile.

What a Commercial Mortgage Calculator Can Tell You

The best calculators give you more than a payment. They show whether the financing structure fits the deal.

For example, for a $1M property at 75% LTV, the loan amount is $750,000. At a 7% rate, 25-year amortization, and a 10-year term, the monthly principal and interest payment is about $5,300, with a balloon payment of around $550,000 due at the end of the term, according to Adventures in CRE at https://www.adventuresincre.com/commercial-mortgage-loan-analysis-model/.

That one output already tells you two things. First, the monthly payment may look reasonable. Second, the future refinance risk may be the primary issue.

Useful outputs that matter in practice

-

Estimated monthly payment

This is the first screening number. It tells you whether the debt service is even in the range of what the property or business can support. -

Amortization pattern

A commercial loan amortization calculator shows how much of each payment goes to principal versus interest over time. -

Total interest cost

Even when the payment feels manageable, the full financing cost may change how attractive the deal looks. -

Balloon payment exposure

If the term is shorter than the amortization, you need to know what balance is still sitting there at maturity. -

Sensitivity to rate changes

A good calculator helps you answer, “What happens if the rate is higher than I hoped?” -

Rough deal fit against income

Payment alone isn’t enough. Lenders care whether the property’s income supports the debt. If you want a clean primer on Debt Service Coverage Ratio (DSCR), that’s worth understanding early because it often determines whether a deal is financeable.

Practical rule: Don’t look at a calculator output and ask only, “Can I make this payment?” Ask, “Does this payment still work after vacancies, repairs, surprises, and family priorities?”

For household-level planning, it also helps to compare the projected payment against your broader cash commitments. A simple family cash flow check like https://alphadadmode.com/how-to-create-a-family-budget/ can keep a “good investment” from becoming a bad pressure point.

Takeaway

A commercial mortgage calculator can tell you whether the debt looks manageable, how the structure behaves over time, and where the hidden pressure points might be.

What a Commercial Mortgage Calculator Cannot Tell You

A calculator gives you a clean estimate. Loans in practice are messier.

The biggest mistake I see is treating the calculator result like an offer. It isn’t. It’s a starting model.

What the calculator usually misses

-

Lender-specific underwriting

A tool doesn’t know how a specific bank or lender views your property type, tenant profile, business strength, or experience. -

Exact closing costs and fees

Advanced underwriting models often break down sources and uses, including closing costs in the 2% to 5% range, as noted by Adventures in CRE at https://www.adventuresincre.com/commercial-mortgage-loan-analysis-model/. A simple commercial loan payment calculator may not include that at all. -

Required reserves

Lenders may require extra liquidity or reserve balances. Most online tools won’t reflect that. -

Credit-driven pricing and eligibility

Commercial lenders often expect a personal FICO score of 680+, with 700 preferred, and business credit markers such as FICO SBSS 140+ and PAYDEX 80+, according to MortgageCalculator.org at https://www.mortgagecalculator.org/calcs/commercial.php. -

Final APR or effective borrowing cost

A quoted interest rate is not the same thing as your all-in cost.

The DSCR gap that trips people up

Many calculators focus on payment math but fail to integrate interactive DSCR analysis. Lenders typically want DSCR of 1.25x or higher, meaning net operating income needs to be at least 25% greater than annual mortgage payments, according to CommercialRealEstate.Loans at https://www.commercialrealestate.loans/commercial-mortgage-calculator/.

That gap matters because it can make buyers think they can borrow more than the property can support.

A payment can look affordable from your perspective and still fail the lender’s cash flow test.

Takeaway

Use the calculator to get direction, not certainty. Then verify fees, reserves, underwriting standards, and property-specific issues with an actual lender or broker.

How to Use a Commercial Mortgage Calculator

A calculator only becomes useful when the assumptions are realistic.

The core formula behind most principal and interest calculations is M = P × [r(1+r)^n / ((1+r)^n – 1)]. For a $400,000 loan at 5% annual interest with a monthly rate of 0.004167 over 240 payments, the monthly principal and interest payment is about $2,639, according to MortgageCalculator.org at https://www.mortgagecalculator.org/calcs/commercial.php.

You don’t need to do that manually. But you do need to understand what each input changes.

Enter purchase price or loan amount

If you know the listing price but not the exact loan, start with the property value and then work backward into a likely loan amount based on your down payment or LTV target.

This gives you a base case. It’s your first estimate, not your final answer.

Add your down payment or LTV assumption

Commercial lending usually requires more equity than residential borrowing. The more cash you put down, the lower the loan amount and the lower the payment.

If you’re using LTV instead of down payment, be honest. A deal that only works with aggressive debt financing may not work in the market.

Enter an interest rate

Rate changes matter fast in commercial deals. Don’t use the lowest rate you’ve seen in marketing copy and call it analysis.

Current lender ranges vary widely. MortgageCalculator.org lists recent commercial ranges such as Freddie Mac Optigo 6.39% to 8.01%, Fannie Mae 6.49% to 7.81%, HUD 223(f) 6.25% to 7.30%, CMBS 6.46% to 7.95%, regional banks and credit unions up to 10.50%, life insurance companies 6.21% to 7.11%, and debt funds 9.07% to 15.32% at https://www.mortgagecalculator.org/calcs/commercial.php.

That spread should tell you something important. Your lender type can matter almost as much as the property.

Choose the amortization period

Amortization controls how long the payment is stretched for calculation purposes. A longer amortization usually lowers the monthly payment.

That can improve near-term cash flow. It can also leave more principal outstanding later.

Choose the loan term

Here, many first-time buyers get tripped up. The term is how long the loan lasts before maturity. The amortization is how long the payment schedule assumes repayment takes.

If the term is shorter than the amortization, the unpaid balance becomes a balloon.

Review the monthly payment

At this stage, the payment is a screening tool. It helps you judge whether the deal deserves more work.

Don’t stop there. Compare that payment against property income, your expected operating costs, and your wider financial obligations. If you want a separate way to keep household cash flow from getting blurred with property math, tools like https://alphadadmode.com/best-budgeting-apps-for-families/ can help organize the non-property side of the decision.

Test multiple scenarios

Run several versions:

- Base case with realistic assumptions

- Higher-rate case to test sensitivity

- More equity case to see if lower debt improves comfort

- Shorter-term case to expose balloon risk

Reality check: A deal that only works under one perfect assumption usually doesn’t work.

Compare with lender estimates

Once the calculator says the deal might make sense, compare your output against lender or broker terms. That’s where you’ll catch underwriting differences, reserve requirements, and fee assumptions.

Commercial Mortgage Calculator Example Scenarios

Examples make the tool more useful because they show what the output means, not just what the fields do.

Small office building purchase

Use a commercial property loan calculator to test a straightforward principal and interest case.

One reference example is a $400,000 loan at 5% interest over 20 years, which produces an estimated monthly payment of about $2,639, with total interest of $233,679 and full cost of $639,679 including fees, based on MortgageCalculator.org at https://www.mortgagecalculator.org/calcs/commercial.php.

What the number means:

The payment might look manageable, but the total financing cost changes how attractive the property is if rents or business income are only modestly above debt service.

Takeaway:

Monthly affordability is only the first layer. Total cost matters if you’re trying to build long-term family wealth rather than just survive the payment.

Owner-occupied storefront or mixed-use property

Many small business owners derive significant value from a calculator in this area.

A calculator lets you compare what happens if you finance conventionally versus testing a government-backed structure. MortgageCalculator.org notes SBA 504 loans at 2.231% to 3.546% APR and SBA 7(a) loans at 5.50% to 11.25% based on July 2020 data at https://www.mortgagecalculator.org/calcs/commercial.php.

What the number means:

Different loan programs can produce very different payment patterns and borrowing costs.

Takeaway:

If you’re buying a property for your own business, don’t compare only buildings. Compare loan programs too.

Multifamily deal with a balloon

A classic commercial real estate loan calculator use case is a loan that looks fine monthly but carries a large maturity balance.

Using the Adventures in CRE example from earlier, a $750,000 loan on a $1M property with a 7% rate, 25-year amortization, and 10-year term results in about $5,300 per month and a balloon of around $550,000 at maturity.

What the number means:

This structure can preserve cash flow now while pushing refinance risk into the future.

Takeaway:

A good monthly payment doesn’t mean a safe loan. It means you need a clear refinance or payoff plan.

First-pass loan sizing from property income

Some advanced models help you size debt by underwriting constraints rather than by payment comfort alone.

PropertyMetrics explains that lenders often size loans using LTV, DSCR, and Debt Yield, then use the lowest resulting loan amount as the binding limit. It gives an example where NOI of $100,000 at a 5% cap rate implies a $2,000,000 value at https://propertymetrics.com/commercial-mortgage-calculator/.

What the number means:

The property’s income and market value can cap your borrowing capacity before your personal comfort level even enters the conversation.

Takeaway:

On commercial deals, “what I can afford” and “what the property can support” are not always the same answer.

Commercial Mortgage Calculator vs Residential Mortgage Calculator

A residential calculator can mislead you if you use it on a commercial deal.

Commercial loans often have different repayment structures, stronger focus on property cash flow, and less standardized fees. That’s why the right tool matters.

| Factor | Residential Mortgage (Your Home) | Commercial Mortgage (Investment/Business Property) |

|---|---|---|

| Loan structure | Often modeled as a long fully amortizing loan | Often includes shorter term structures, interest-only periods, or balloons |

| Term and amortization | Often treated as one timeline in simple calculators | Often separate, which can create a remaining balance due at maturity |

| Underwriting focus | Heavier focus on personal income and consumer credit | Strong focus on property income, deal structure, and lender metrics |

| Down payment expectations | Often lower in consumer lending | Commonly higher, with many scenarios requiring meaningful equity |

| Fees and reserves | More standardized consumer-style expectations | More lender-specific and harder to estimate with a basic tool |

| Property analysis | Homeownership affordability lens | Investment and operating-performance lens |

A residential calculator is fine for rough payment math. It’s not enough for a commercial acquisition.

That difference is similar to comparing short-term rental economics and long-term rental economics. The property may be real estate in both cases, but the decision framework changes. A simple comparison like https://alphadadmode.com/airbnb-vs-vrbo/ shows how the same asset class can require very different assumptions.

Best Tools and Calculators for Commercial Mortgage Analysis

The best tool depends on what you’re trying to answer.

Basic payment calculators

Best for: First-pass affordability checks

Key benefit: Fast principal and interest estimates

Limitation: Often too shallow for underwriting-level analysis

Why it may help: Useful when you’re screening listings quickly

MortgageCalculator.org is a practical example. It handles commercial-style structures and gives clean payment outputs without much friction.

Balloon and amortization-focused calculators

Best for: Buyers comparing term versus amortization trade-offs

Key benefit: Shows future balance risk, not just monthly payment

Limitation: May still omit broader deal assumptions

Why it may help: Better for loans where maturity risk matters as much as monthly affordability

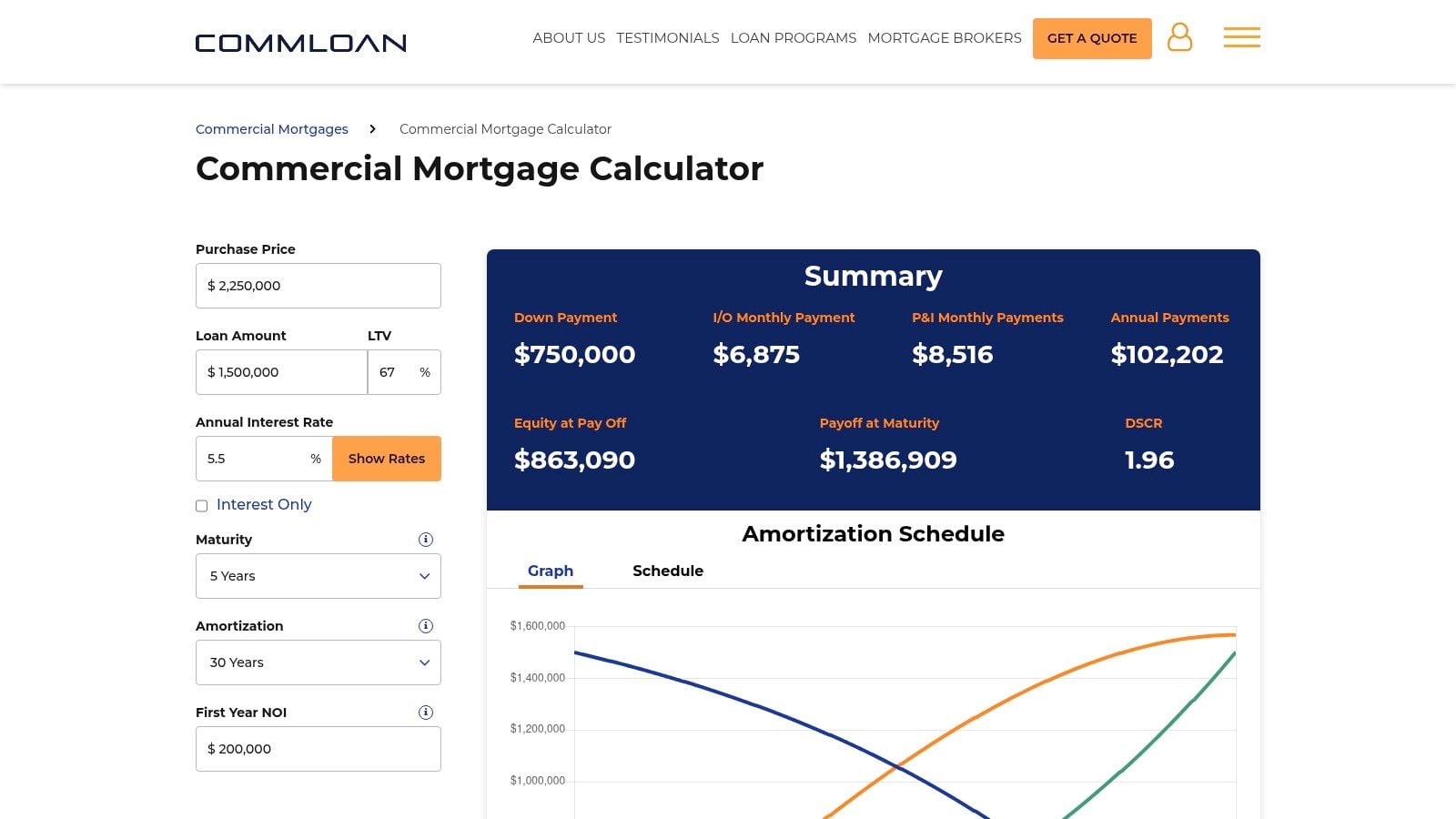

CommLoan’s calculator is useful when you want to think more like a lender and less like a casual browser. If you’re comparing a few deal structures, this is the kind of tool worth testing.

Underwriting and sizing models

Best for: Investors who want to evaluate whether the property qualifies on lender metrics

Key benefit: More attention to LTV, DSCR, and Debt Yield

Limitation: More inputs means more room for user error

Why it may help: Better for buyers who are moving beyond “What’s the payment?” into “Will this deal clear credit standards?”

PropertyMetrics notes that lenders prioritize Debt Yield for some non-recourse loans, and common benchmarks in major markets include LTV of 65% to 75%, DSCR of 1.25x to 1.50x, and Debt Yield of 8% to 12% at https://propertymetrics.com/commercial-mortgage-calculator/.

Use a basic calculator to screen deals. Use a deeper model when you’re serious enough to submit terms or make an offer.

Investment analysis spreadsheets and templates

Best for: Buyers who want full control over assumptions

Key benefit: Flexible scenario testing

Limitation: Takes more time and some spreadsheet discipline

Why it may help: Good if you want to combine financing with rent assumptions, expenses, and exit thinking

For projects that move beyond a simple purchase and into heavier planning, it can also help to understand how broader feasibility tools work. This overview of property development appraisal software is useful context if your analysis is becoming more detailed than a standard online calculator can handle.

Lender marketplaces and quote platforms

Best for: Borrowers ready to compare options after initial modeling

Key benefit: Moves from theory toward actual lender appetite

Limitation: Quotes still aren’t final approvals

Why it may help: Good next step once your numbers hold up under stress

Who should skip which tool

- Skip the basic calculator if you’re already evaluating cash flow, refinance risk, and lender thresholds.

- Skip the advanced model if you don’t yet have dependable income and expense assumptions.

- Skip lender marketplaces until your own assumptions are organized and realistic.

Soft CTA: If you only need a fast estimate, start with a simple commercial mortgage payment calculator. If the deal still looks good, move up to a stronger underwriting model before you talk to lenders.

Common Mistakes When Using a Commercial Mortgage Calculator

Most calculator mistakes are assumption mistakes.

Treating the payment like the full cost

The payment is only one layer of ownership cost. Fees, legal costs, reserves, taxes, insurance, and operating expenses can change the complete picture quickly.

A clean output can create false confidence if you don’t add the rest of the stack.

Ignoring the balloon

Commercial borrowers often focus on the monthly payment because it’s easy to compare. The maturity balance is where trouble can hide.

If your term is shorter than your amortization, the calculator isn’t finished until you’ve looked at the remaining balance.

Using a best-case interest rate

This is one of the most common errors. CommLoan notes that commercial loans often carry spreads of 50 to 100 basis points over benchmarks, which can increase payments by 10% to 15% relative to optimistic online quotes, and it recommends stress-testing with a 2% rate increase at https://www.commloan.com/commercial-mortgages/calculator.

That’s practical advice. If the deal breaks under a rate shock, you’ve learned something useful before spending money on third parties.

Confusing term with amortization

A lot of first-time buyers accidentally use a residential mindset here. They assume the loan term equals the payoff period.

Commercial financing often separates them. That changes both risk and exit planning.

Forgetting to test downside scenarios

Run the base case. Then run a worse case.

Better question: Not “What does the calculator say today?” but “What still works if the loan is less favorable than I hoped?”

If the property only works when every assumption is generous, that’s not conservative analysis. That’s wishful thinking.

Who Should Use a Commercial Mortgage Calculator

This tool is useful for more people than just full-time investors.

-

First-time commercial buyers

Good for understanding whether a property is even worth deeper underwriting. -

Experienced investors

Helpful for comparing structures quickly before moving into full analysis. -

Owner-occupant business buyers

Useful when deciding whether buying space makes more sense than staying a tenant. -

Multifamily buyers

Good for checking payment structure and refinance exposure. -

Brokers and deal screeners

Useful for fast preliminary numbers before building a deeper package. -

Anyone trying to learn the language of commercial lending

A calculator makes abstract terms more concrete. If you’re building that foundation, practical reading like https://alphadadmode.com/best-real-estate-books/ can also help you sharpen your judgment.

Frequently Asked Questions

How accurate is a commercial mortgage calculator

It’s usually accurate for estimating payment math if the inputs are accurate. It is not a final loan quote or approval decision.

What is the difference between loan term and amortization

The term is when the loan matures. The amortization is the schedule used to calculate how long repayment would take. If the term is shorter, you may owe a balloon balance at maturity.

Can a commercial mortgage calculator estimate balloon payments

Yes, if it allows you to enter a separate term and amortization period. Basic calculators may not handle this well.

What costs are not included in most calculators

Many calculators don’t fully include lender fees, legal costs, reserves, prepayment terms, taxes, insurance, or the full operating cost of the property.

Is a commercial mortgage calculator enough to compare lenders

It’s a good first step, but not enough by itself. Lenders differ on pricing, underwriting, reserves, and property preferences.

How much down payment do commercial loans usually require

It varies by lender and deal structure. Many buyers should expect to contribute meaningful equity rather than rely on low-down-payment residential assumptions.

Can I use a residential mortgage calculator for commercial property

You can use one for a rough payment estimate, but it may miss critical features like balloon structures, interest-only periods, and commercial underwriting assumptions.

What should I compare after using the calculator

Compare the payment, balloon risk, all-in cash required, property income support, and whether the loan still works under less favorable assumptions.

Your First Step to a Smarter Investment

A commercial mortgage calculator is one of the best first-step tools in commercial real estate because it forces the deal into numbers fast. That alone saves time, bad assumptions, and avoidable excitement.

It’s still only a starting point. The smart move is to use the calculator to compare scenarios, identify pressure points, and show up to lender conversations prepared. If the deal works under realistic assumptions, then it’s worth taking to the next level.

If you want more practical, no-fluff guidance on money, real estate thinking, and making stronger long-term decisions for your family, visit alphadadmode.com. It’s built for dads who want to lead with clarity, not guesswork.